The obligation to register to pay VAT in another Member State

Exporting online stores often ask us if they are required to establish a local companies in certain states if expanding the online store to the foreign, what is actually the obligation to register to pay VAT in the foreign and so on. Therefore we decided to write an article that clarifies this topic. Let’s do it in order.

If you ask whether you are required to immediately establish a local company when expanding, then our answer is NO, you are not. However, you have to look at this issue more pragmatically. If your company is based in Eastern Europe, we recommend to establish a local company in Western Europe (mainly in countries such as Germany, Austria, and Switzerland). What is a reason? For example, German customers are very sensitive to companies from this Eastern Europe and they show relatively high level of mistrust.

If I do not establish a local company, how is it with VAT payment?

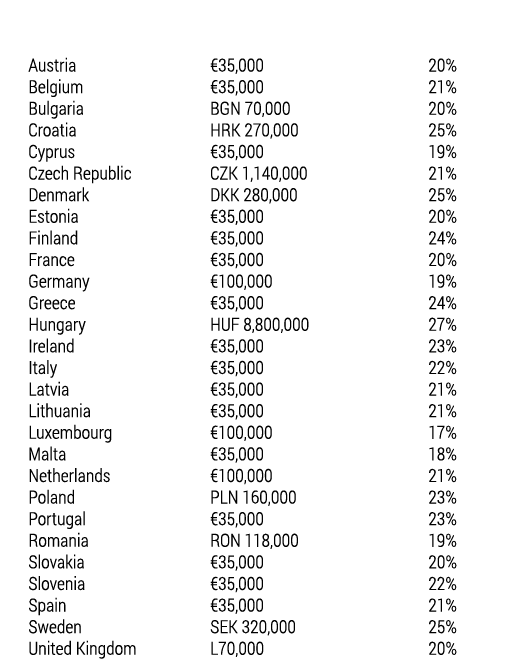

In order to help reduce the administrative burden on companies and encourage them to start trading across Europe, there are national thresholds for VAT registration that are set by each country in particular. If a foreign company sells under the thresholds mentioned below, VAT records are not required. However, when you exceed these limits within the same calendar year, you must apply for registration of VAT payer in the EU.

Example:

Let's imagine the situation of a Slovak online store, which starts selling goods in Hungary. At the beginning, invoices will include Slovak VAT (20%). At the moment when you exceed the limit 35,000 € in Hungary, you are required to register to pay Hungarian VAT.

For entrepreneurs, the fact that there are no tax frontiers between individual EU Member States, on the one hand means the extension of possibilities of their business activities, on the other hand, it may also mean some financial loss caused by lack of knowledge and insufficient knowledge of tax laws valid in other states. Actual practice shows that VAT has become a particularly risky area for entrepreneurs in given direction. Therefore, it is adequate to contact companies, which consider tax consultancy as a key service for customers that are also thinking about expanding abroad.

From the principles valid for the single market of the European Union anchored in the Sixth Council Directive no. 77/388 / EEC results that in case if a taxable person carries out such taxable business in which the condition of registration in another Member State is met, is required to register in the State, where is the place of taxable business.

Make sure to check that the customer you sell to, is actually within the EU’s VAT. Some locations that are part of the EU are outside the EU's VAT area (e.g. Åland, which is part of Finland but is outside of the EU’s VAT) and other non-EU regions are considered to be EU territories (e.g. Monaco).

If you have any questions, Expandeco is here for you any time.

Values for the registration of VAT payer in individual countries: