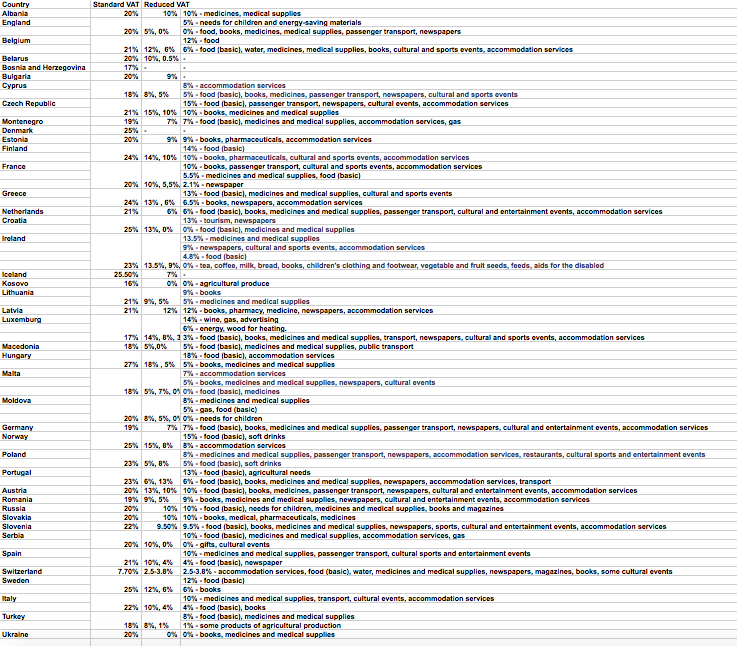

What VAT rates do EU Member States have in 2019?

VAT is applied throughout the European Union, but each country determines its value separately, so VAT rates vary across EU countries.

There are standard VAT rules in the EU, but the VAT law can also be applied in different ways in individual countries. Usually you have to pay VAT on all goods and services, including sales to the final consumer, which everyone who thinks of expanding abroad should think of.

For EU-based companies, VAT is charged on most sales and purchases within the European Union. VAT is not charged on export to non-EU countries. In this case, VAT is paid in the importing country.

The following VAT rates apply in the Member States of the European Union in 2019:

- standard VAT rate

- reduced VAT rates

- special VAT rates

Standard VAT rate

The base rate applies in most cases and is applied by every EU Member State. It is determined as a percentage of the tax base and is the same for the supply of goods and services. The standard VAT rate may not be less than 15%.

Reduced VAT rates

EU countries can apply one or two reduced VAT rates. The reduced rates shall apply only to the supply of goods or services referred to in Annex III. Council Directive on the common system of value added tax. However, they do not apply to electronically supplied services.

The reduced VAT rate can be applied in Member States, for example to:

* foods except alcoholic beverages

* some pharmaceutical products

* medical equipment

* delivery of books

* services provided by artists and copyright fees

Reduced rates do not apply to electronically supplied services.

Reduced rates are set as a percentage of the tax base and may not be less than 5%.

Special VAT rates

Some EU countries apply specific VAT rates to some goods and services, for example:

* Super reduced VAT rate: Applies, for example, of 4% in Spain for the supply of services such as the maintenance and modification of vehicles for people with disabilities

* Zero rate: The consumer does not have to pay any VAT, but the seller has the right to deduct the VAT he paid on purchases directly linked to the sale

* "Parking" or transition rate: Applies to certain goods and services that are not eligible for a reduced rate but for which some EU countries have already applied reduced VAT rates since 1.1.1991.

Source: Alavara.com